In-app payments are on the rise- but how can you make them work for your business? Anna Tsyupko, CEO at Paybase, looks at the key challenges of integrating payments within your app.

Building a payments component into your app can be more complicated than you might expect.

Platforms such as online marketplaces or FinTech apps require electronic money (eMoney) infrastructure because they have complex requirements that cannot simply be accommodated by a payment gateway. These types of businesses need to issue money to individual merchants or users and the ability to transfer money between accounts or rather than simply process inbound payments.

EMoney infrastructure allows for the easy opening of eMoney accounts – lightweight financial instruments – in-app or directly on your website. This makes it perfect for escrow-like accounts, peer-to-peer-transactions and attached physical prepaid cards to name but a few applications.

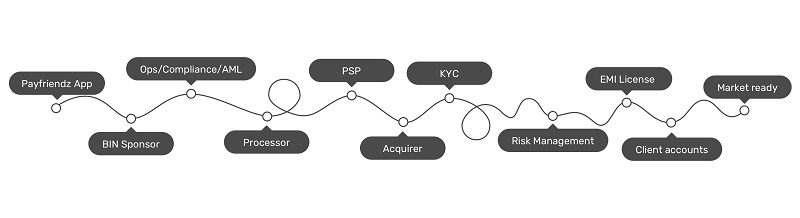

Unfortunately eMoney infrastructure is expensive and time-consuming to put in place, as we discovered when building our peer-to-peer payments app, Payfriendz. We were unable to find a secure, modern, tech-first payments partner that could deliver payment solutions and handle compliance and risk. Existing providers in the field are not flexible enough to support innovative use cases, so we had to build our own payments infrastructure.

Here are the challenges we faced along the way.

- Regulatory cover

In order to issue eMoney, you have to be licensed as an eMoney Institution (EMI) by the Financial Conduct Authority. It can take up to six months to prepare the application and up to another six months to get approved.

In the current market, this is a lifetime. A lifetime that could be better spent on your core business.

If you want to issue not only eMoney but also physical or virtual pre-paid payment cards, you either need to get an issuing licence for Visa or Mastercard (high cost, long time frame), or find a BIN (Bank Identification Number) sponsor who will allow you to operate under their licence.

Finding a suitable BIN sponsor is not straightforward. A BIN sponsor will only grant you the cover you need once you can prove that your organisation has the experience needed to operate a financial product and manage all the intricacies around fraud, risk management, operational flows, etc. If you don’t have this expertise already, you will need to look at hiring a person or assembling a team that does.

2. Risk management and fraud prevention

You can plan and test for many eventualities, but you can never completely understand ‘typical user behaviour’ – let alone fraudulent user behaviour – until you have an active user base. We had to spend a lot of time going down the trial and error route until eventually we started seeing patterns and finding ways to best prevent misuse.

The legacy partners we engaged with offered transaction monitoring tools and services, but they were not flexible enough to support our use case. To solve this problem, we designed and built our own tools in house, costing us more time, resources and money.

3. Risk, KYC, and Identity Verification Providers

Risk, Know Your Customer (KYC) and Identity Verification providers help businesses verify clients’ identities, ensuring anti-money laundering regulatory requirements are upheld.

Choosing the right KYC provider for your business can be a challenge. The KYC provider we worked with originally led to low pass rates. At one point as many as 40% of our customers were not passing the checks as our student customer base had minimal credit history due to their age.

After extensive research and trials of different providers, we came to know the KYC provider market well and understood that we needed a provider that was well placed to verify younger customers.

Extensive expertise in the payments industry is required in order to get these things right the first time, which is critical when your business depends on payments.

4. Integration with partners

Along the way we had to integrate with many different service providers in order to meet our requirements. These included a BIN sponsor, processor, KYC provider, Payment Service Provider (PSP), Acquirer and Banking Partner.

Managing many integrations with third party providers is extremely time-consuming. We had to project manage all integrations and account for dependencies (e.g. not all BIN sponsors and Processors can work together out of the box), and each integration needed thorough testing.

Our launch marketing push meant huge user base growth and a sudden increase in required capacity, which some of our partners struggled with. This was highly frustrating after having worked so hard to make sure the set-up was perfect before launch.

5. Contract length and costs

Most of the providers have high set-up fees, monthly minimum commitments and long contract terms. Often these high fees do not include changes in scope and requirements – something that legacy partners struggle to provide within reasonable time. Some of our requirements were not supported ‘out of the box’, meaning we had to pay extra and wait for weeks, sometimes even months, for these changes to go live.

In summary, throughout the process of developing a simple peer-to-peer payments app, it became very apparent that many payments partners are still set up to support the old-fashioned payments world, not the new, innovative FinTech companies that are quickly emerging.

Going through this experience gave us invaluable first-hand insight. We have applied this insight to create something truly different which will help other businesses avoid the struggles we had to face.

We distilled all our knowledge and experience into the Paybase Platform that offers a simple, yet flexible, single integration covering payments, compliance and risk. Built using the latest technology, the Paybase Platform has no prohibitive set-up fees, enabling innovation from small and mid-size companies that would normally struggle to afford such infrastructure. Paybase can help these companies get to the market more quickly by providing a complete end-to-end solution with just one touchpoint.

Find out more on our website or email us to let us know what you are working on.